- Companies growing at > 20% top line

- Significant growth drivers include international expansion

Monthly Archives: April 2016

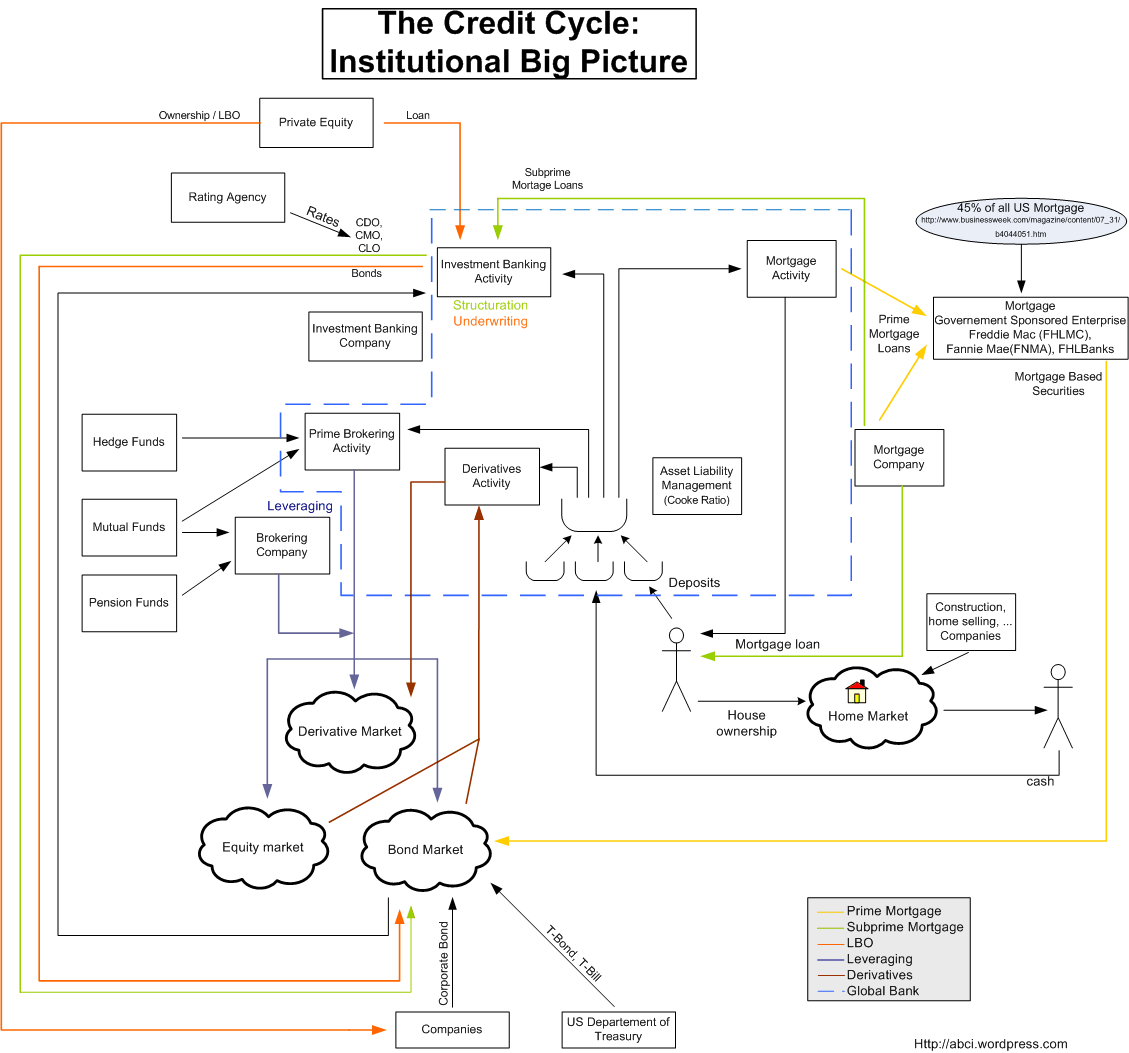

Austrian Business Cycle

Commercial banking money:

Initial Observations on Skechers (SKX)

Derived from Piotroski screen

Observations

- Trading at less than 50% of its 52-week high resulting from missing Q3 earnings

- International sales comprises of 40% of revenue, near its 50% target

- Correction (presumably) derives from negative sentiment associated with soft consumer discretionary products (driven by low oil prices) for Apparel, Accessories and Footwear

- Revenue growth of > 20%

- $4.5bn market cap, net debt negative

- Relatively cheap shoes (versus Under Armour, Nike)

- NTM P/E: Current of 13.5x; Average of 19x; High of 28x

- EPS expected to double from $1.50 / sh to $3.00 / sh

Analyze

- Dividends / repurchases

- Sensitize EPS

First Look: Mylan

Observations

- Has portfolio of over 1,400 drugs

- Mylan down 30% YoY

- Share price declined from ~$70 / sh to ~$40 / sh following rejection of takeover bid by Teva ($82 / sh)

- Acquired Meda for $7.2bn

- Multiple compression in late 2015 due to attempts to acquire Perrigo

- 2018E EPS of $6.00 / sh, (2016E $5.92 / sh)

- NTM EPS Average of 12x; Current of 10x; High 18x

- Ranked #1 for generics sales

- Mylan is a beneficiary of the patent cliff for branded drug companies

- 45% of revenue is from international markets

Considerations

- High revenue and profitability growth – what does terminal state look like?

- To what degree is management distrust warranted?

- What is management’s strategy for shareholder payout?

Analyze

- Return on capital over 8 years

- CFO / Total assets for 8 years

Reference Material

- Emily Muhleman on Seeking Alpha

Valuing Franchises

Greenblatt Return on Capital (EBIT / Capital)

- Capital: Net PP&E + Net Working Capital

- or Fixed assets + current assets – current liabilities – cash

Price to Tangible Book Value Screen

- Price / Tangible Book Value (Total Assets – Intangible Assets – Total Liabilities) < 1

Observations: energy companies & other natural resources prevalent. Micron appears too. 29 companies total

Tobias Carlisle on Liquidation Value

The assets of a company are typically worth more as part of a going concern than in liquidation, so liquidation value is generally a worst-case outcome. In m experience, most ‘net net’ companies have been turned around, rather than liquidated.

Mohnish Pabrai on Valuation

I value [consistency] of earnings more than the absolute cheapest business, because then we know there is some sustainability to the cheap business getting even cheaper, and eventually gravity takes over.

Net Working Capital Screen

Developed a screen *proxy* for Graham style net net value (NWC – total debt) by utilizing NWC only.

- NWC > Market Capitalization

Observations: most companies laden with net debt (of 8 companies) based on companies ranging from 2bn – 15bn on major US exchanges.

Piotroski Screen

- Piotroski score of 8 or 9

- < 75% of 52-week high

Notable Equities:

- Kate Spade – growth play from break-even PE; however bottomed in February 2015

- Skechers – missed Q3 results resulting in 50% decline; strong growth at $3.2bn revenue (~$200mm Net Income equivalent to 7% margin; EPS expected to double by 2018); international growth focus