In the spirit of object-driven visualization: segmenting markets on the basis of sectors I do / do not have exposure to and key themes I’m currently following.

per Shiller

Given the volatiltiy resulting from the unexpected Brexit vote, I’ve logged a few important considerations associated with SP500 valuations during the next few months:

Direct Effects

Related “Swing” Factors

Most importantly, investors will have to factor in a higher chance of a stagflationary outcome over the next three to five years: even lower growth or near-stagnation coupled with a significant rise in inflation

- Current or future governments turn more protectionist by erecting barriers to trade and migration…

- …and take up or intensify the battle against inequality by redistributing income (through taxation and regulation) from capital to labor.

Source: Barrons (June 2016)

Source: McKinsey (June 2013)

Source: McKinsey (May 2015)

The Chinese consumer is evolving. Gone are the days of indiscriminate spending on products. The focus is shifting to prioritizing premium products and living a more balanced, healthy, and family-centric life.

Source: McKinsey (March 2016)

While these are positive moves, there are still improvements that need to be made in high speed mobile data and security as heavy data usage will require more 4G/LTE antennas and IT infrastructure across the region.

– Shafiq Arghandiwal, Director of Technology, Matthews Asia

Identify beneficiaries of telecom and IT infrastructure companies in Asia

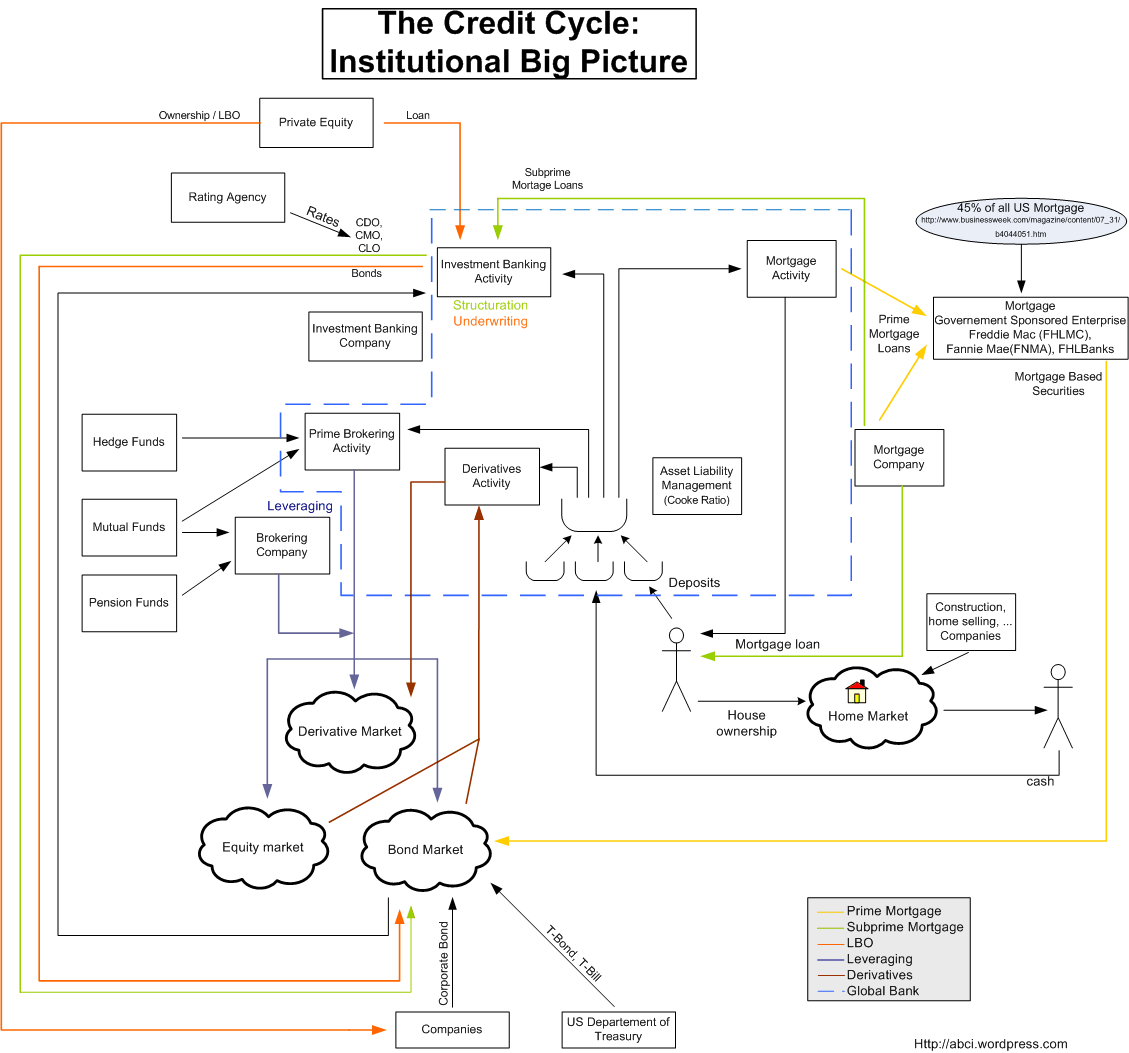

Commercial banking money: